MUTUAL FUND

![]()

![]()

![]()

![]()

![]()

![]()

Click the above-mentioned AMC Logo to Invest Online directly into the Mutual Fund AMC's scheme.

Click the above-mentioned AMC Logo to Invest Online directly into the Mutual Fund AMC's scheme.

About Mutual Fund

# What is a Mutual Fund?

To many people, Mutual Funds can seem complicated or intimidating. We are going to try and simplify it for you at its very basic level. Essentially, the money pooled in by a large number of people (or investors) is  what makes up a Mutual Fund. This fund is managed by a professional fund manager.

what makes up a Mutual Fund. This fund is managed by a professional fund manager.

It is a trust that collects money from a number of investors who share a common investment objective. Then, it invests the money in equities, bonds, money market instruments, and/or other securities. Each investor owns units, which represent a portion of the holdings of the fund. The income/gains generated from this collective investment is distributed proportionately amongst the investors after deducting certain expenses, by calculating a scheme’s “Net Asset Value or NAV. Simply put, a Mutual Fund is one of the most viable investment options for the common man as it offers an opportunity to invest in a diversified, professionally managed basket of securities at a relatively low cost.

# What are the benefits of investing in Mutual Funds?

Many of us dread the thought of managing our own investments. With a professional fund management company, people are put in charge of various functions based on their education, experience, and skills.

As an investor, you can either manage your finances yourself or hire a professional firm. You opt for the latter when:

- You do not know how to do the job best – many of us hire someone to file our income tax returns, or almost all of us get an architect to do our house.

- You do not have enough time or inclination. It’s like hiring drivers even though we know how to drive.

- When you are likely to save money by outsourcing the job instead of doing it yourself. For going on a journey driving your own vehicle is far costlier than taking a train.

- You can spend your time on other activities of your choice/liking.

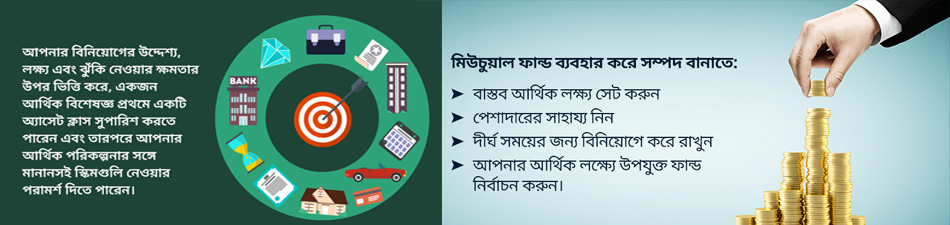

Professional fund management is one of the best benefits of Mutual Funds. The infographic on the left highlights all the others. Given these benefits, there is no reason why one should look at any other investment avenue.

# Why is investing better than saving?

Imagine a 50-over cricket match in which the #6 batsman walks into bat only in the 5th over. His job is to first ensure he does not lose the wicket, and then focus on scoring runs.

While saving is a must for investing, it is important to save one’s wicket in order to be able to score later. One can save the wicket by playing defensive cricket and avoiding all sorts of shots. But that would result in a very low score. He would need to hit some boundaries by taking certain risks like lofted shots or drives between fielders or cuts and nudges.

Similarly, in order to accumulate large sums to meet one’s financial goals, in order to beat inflation, one must take certain investment risks. Investing is all about taking calculated risks and managing the in same way, not avoiding the risks altogether.

At the same time, in the cricket analogy, in order to stay at the crease as well as score runs, one must take calculated risks and not play rash shots. Taking unnecessary risks is a bad strategy.

So, while saving is necessary, investing is very important to achieve long-term goals.

# Aren’t RDs and FDs enough to secure the future?

Recurring Deposits (RDs) and Fixed Deposits (FDs) are some of the most popular savings instruments in our country. They are safe and offer a guaranteed rate of return.

Recurring Deposits (RDs) and Fixed Deposits (FDs) are some of the most popular savings instruments in our country. They are safe and offer a guaranteed rate of return.

That really depends on what an investor expects from the future. If the investor wants her capital to be safe and earn some reasonable fixed rate of return, irrespective of inflation and taxes, then these may be good enough. However, if the investor wants to earn a positive return even after factoring in inflation and taxes, then these may not be good enough.

If an investor has a large enough corpus to start with and is really not worried about enhancing purchasing power, then RDs and FDs are safe and useful savings and income-generating options. If an investor is more concerned about the safety of the principal and receipt of timely and predictable income, an FD may be ideal.

# Why should one invest in Mutual Funds?

One should never invest in Mutual Funds but should invest through them.

One should never invest in Mutual Funds but should invest through them.

To elaborate, we invest in various investment avenues based on our requirements, e.g., for capital growth - we invest in equity shares, for the safety of capital, and for regular income - we buy fixed-income products.

The concern for most investors is: how to know which instruments are best for them. One may not have enough abilities, time, or interest to conduct the research.

To manage investments, one can outsource certain tasks one is unable to do. Anyone can outsource ‘managing one’s investments to a professional firm – the Mutual Fund company. Mutual Funds offer various avenues to fulfill different objectives, which investors can choose from based on one’s unique situations and objectives.

Mutual Fund companies manage all administrative activities including paperwork. They also facilitate accounting and reporting the progress of the investment portfolios through a combination of Net Asset Values (NAVs) and account statements.

Mutual Fund is a great convenience for those who need to invest their money for future requirements. A team of professionals manages the money, and the investors can enjoy the fruits of this expertise without getting involved in mundane tasks.

# What are the indicators of risk in a Mutual Fund Scheme?

You must properly evaluate before picking up the right Mutual Fund scheme to invest your hard-earned money. While investors often go by scheme category and top-performing schemes in the category, they ignore risk indicators for these schemes. When you are comparing schemes to choose from, don’t miss out on comparing their riskiness. While there are many risk indicators like Standard Deviation, Beta, and Sharpe Ratio provided in the factsheet of every scheme, the product label is the most basic thing to look for. The risk-o-meter on the label shows the risk level of the fund. This risk-o-meter is a mandatory requirement by SEBI and represents the underlying risk associated with the fund. The six levels of risk ranging from low, low to moderate, to moderate, moderately high, high, and very high have been linked to various categories of mutual funds depending on the level of risk in their portfolio. Since this kind of risk categorization has been defined by SEBI, all mutual funds are bound to categorize similar kinds of funds into the same risk category.

Apart from the risk-o-meter which gives an overview of the fund’s riskiness, one can also look at more specific risk indicators provided in the factsheet. Standard Deviation measures the range of a fund’s return. A scheme with a higher standard deviation of return indicates its range of performance is wide, implying greater volatility.

Beta measures a fund’s volatility with respect to the market. Beta >1 implies the scheme will be more volatile than the market and Beta<1 means it’ll be less volatile than the market. A beta of 1 indicates the scheme will move in tandem with market volatility.

Sharpe Ratio measures the excess return provided by the fund per unit of risk undertaken. It is a good indicator of risk-adjusted return.

Next time you research which scheme to invest in, don’t forget to evaluate them on the above risk parameters.

Risk In Mutual Fund

# Are all Mutual Funds risky?

Every investment we make involves a risk, only its nature and degree varies. The same applies to Mutual Funds too.

Every investment we make involves a risk, only its nature and degree varies. The same applies to Mutual Funds too.

All Mutual Fund schemes do not carry the same risk when it comes to returns on investment.

Equity schemes have the potential to deliver superior returns over the long term that can create wealth. Remember, inflation is a risk, and equities are the best asset class to beat inflation. So, in a sense, there are some risks that are worth taking.

On the other hand, the risk associated with liquid funds is significantly low when compared to equity funds. A liquid fund focuses on the protection of capital by taking lower risks and generating returns in line with the risk taken.

It is also important to remember that the risk on returns is not the only risk you need to consider. There are other risks – liquidity risk for instance. Liquidity risk measures the ease of converting your investment into cash. This risk is lowest in Mutual Funds.

In the end, the nature and extent of risk are best understood through proper understanding and evaluation of the scheme and by taking the guidance of a Mutual Fund distributor or an investment advisor.

# What are the various types of mutual funds?

Various types of Mutual Fund schemes exist to cater to the different needs of different people. Largely there are three types of mutual funds.

Equity or Growth Funds

- These invest predominantly in equities i.e., shares of companies.

- The primary objective is wealth creation or capital appreciation.

- They have the potential to generate higher returns and are best for long-term investments.

- Examples would be.

- “Large Cap” funds invest predominantly in companies that run large established businesses.

- “Mid Cap funds” invest in mid-sized companies. funds that invest in mid-sized companies.

- “Small Cap” funds that invest in small-sized companies.

- “Multi Cap" funds” are funds that invest in a mix of large, mid, and small-sized companies.

- “Sector” funds invest in companies that are related to one type of business. E.g., Technology funds that invest only in technology companies.

- “Thematic” funds that invest in a common theme. E.g., Infrastructure funds invest in companies that will benefit from the growth in the infrastructure segment.

- Tax-Saving Funds

Income or Bond or Fixed Income Funds

- These invest in Fixed Income Securities, like Government Securities or Bonds, Commercial Papers and Debentures, Bank Certificates of Deposits, and Money Market instruments like Treasury Bills, Commercial papers, etc.

- These are relatively safer investments and are suitable for Income Generation.

- Examples would be Liquid Funds, Short Term, Floating Rate, Corporate Debt, Dynamic bonds, Gilt Funds, etc.

- These invest in both Equities and Fixed Income, thus offering the best of both, Growth Potential as well as Income Generation.

- Examples would be Aggressive Balanced Funds, Conservative Balanced Funds, Pension Plans, Child Plans and Monthly Income Plans, etc.

# Is Choosing a Mutual Fund too confusing?

Yes, there are several types of Mutual Fund schemes – Equity, Debt, Money Market, Hybrid, etc. And there are many Mutual Funds in India managing several hundreds of schemes amongst them. So it may appear that zeroing in on a scheme is actually a very complex and confusing affair.

Choosing the scheme to invest in should be the last thing on an investor’s mind. There are several more important steps before that, which will help remove much confusion later.

Choosing the scheme to invest in should be the last thing on an investor’s mind. There are several more important steps before that, which will help remove much confusion later.

An investor should, first of all, have an investment objective, say retirement planning or renovating one’s house. The investor has to arrive at two figures – how much would this cost and how long it would take, while also knowing how much risk can be taken.

In other words, based on an investor’s goals and objectives and risk profile, a type of fund is recommended, say equity or hybrid, or debt, and only then specific schemes are selected, based on track record, portfolio fit, etc.

In essence, if there is clarity of investment purpose in the beginning, there would be a lot less confusion about the choice of the fund in the end.

# Can Mutual Funds help create wealth?

Business and commerce allow us to create wealth by investing our money with those who are on the path to creating wealth. We can be investors in the businesses of entrepreneurs, by investing in stocks of various companies. As entrepreneurs and managers run their businesses efficiently and profitably, the shareholders get the benefits. In this regard, Mutual Funds are a great way to build wealth.

But how do we know which stocks to buy, and when?

That is where taking professional help counts. They also take advantage of a large corpus to explore more opportunities simultaneously. Like a balanced diet – we all need proteins, vitamins, carbohydrates, etc. Eating only one type results in some nutrient deficiency. Similarly, in a diversified equity fund you’re exposed to different segments of the economy, and also protected from the potential downside.

Invest in a professionally managed, diversified equity fund and stay invested for a long period to create wealth for yourself and your next generation.

# What are the various types of debt funds?

Debt funds are for investors who seek the safety of capital or regular income from investment and/or want to park money for short periods.

But debt funds are of various types.

Like in banks, you can open a savings account, where you can put and remove money whenever you want. However, it doesn’t make sense to keep money idle, if you are not likely to use it for some time. You may, in such a case, open a fixed deposit – where the money is locked in a certain period allowing you to earn a higher rate of interest. You may also opt for a recurring deposit, wherein you keep investing a fixed amount every month for a pre-defined period of time. All these products help you with different requirements.

Similarly, among Mutual Funds too there are variants available in the debt fund category to fulfill various needs of investors, like – Liquid Funds, Income Funds, Government Securities, and Fixed Maturity Plans. An investor would be advised to select schemes based on one’s unique requirements.

# Can one invest in multiple asset classes using one Mutual Fund scheme?

Mutual Fund schemes investing in a single asset category are like specialist bowlers or batsmen. Whereas certain other schemes, known as hybrid funds, invest in more than one asset category, e.g., some invest in equity and debt. Some may also invest in gold apart from equity and debt.

category, e.g., some invest in equity and debt. Some may also invest in gold apart from equity and debt.

In cricket, we see batting all-rounders as well as bowling all-rounders depending on the skill, they are better at. Similarly, there are Mutual Fund schemes that invest heavily in one asset category as compared to another.

The oldest category, the balanced fund category, invests in equity and debt. The allocation to equity is normally higher (over 65%) and the rest is in debt.

The other popular category is known as MIP or the monthly income plan endeavors to provide monthly (or regular) income to investors. However, there is no guarantee of regular income. These schemes invest predominantly in debt securities so that regular income can be generated. A small portion is invested in equity to enhance returns over the years.

Another variation of the hybrid scheme invests in equity, debt, and gold, to take advantage of three different asset classes in one portfolio.

An investor has an option of buying different equity or debt or gold fund schemes to create a hybrid portfolio or alternately buy a hybrid fund.

# Are Mutual Funds ideal for short-term or long-term Investment?

“Mutual Funds could be a good saving tool for the short term.”

“You must be patient with your Mutual Fund investments. It takes time to deliver results.”

People regularly come across both the above statements, which are clearly contradictory.

So what period are Mutual Funds suitable for? Short-term or long-term?

Well, that depends on what one’s investment goals are, and most goals are driven by time. There are schemes suitable for short periods, there are several schemes suitable for a longer horizon, and then, there are schemes for any period in-between.

Well, that depends on what one’s investment goals are, and most goals are driven by time. There are schemes suitable for short periods, there are several schemes suitable for a longer horizon, and then, there are schemes for any period in-between.

Consult your Mutual Fund distributor or your investment advisor, discuss your financial goals, and then decide where you want to invest. For example.

- A. Equity-oriented Mutual Funds- Look for longer periods, typically 5 years and above.

- B. Fixed Income oriented Mutual Funds-

- 1. Liquid Funds - For very short term – Less than 1 year

- 2. Short-Term Bond Funds – For the medium term – 1 to 3 years.

- 3. Long-Term Bond Funds - For the long term – 3 years or more

As you explore our website, you will learn more about the various kinds of Mutual Funds too. Your mutual fund distributor/investment advisor can also help you identify the right type of MF to invest in as per your goals!

More details about Mutual Fund

# Why invest in gold mutual funds when we can invest in gold ETFs?

A Gold ETF is an exchange-traded fund (ETF) that aims to track the domestic physical gold price. They are passive investment instruments that are based on gold prices and invest in gold bullion. In India, Gold is usually held in ornament form, which has a certain making and wastage component (usually more than 10% of the bill value). This is eliminated when investing in a Gold Fund.

Buying gold ETFs means you are purchasing gold in an electronic form. You can buy and sell gold ETFs just as you would trade in stocks. When you actually redeem Gold ETF, you don’t get physical gold but receive the cash equivalent. Trading of gold ETFs takes place through a dematerialized account (Demat) and a broker, which makes it an extremely convenient way of electronically investing in gold.

Because of its direct gold pricing, there is complete transparency on the holdings of a Gold ETF. Further due to their unique structure and creation mechanism, ETFs have much lower expenses as compared to physical gold investments.

# What are some mistakes people make when investing in Mutual Funds?

Making a mistake while investing happens across all investments, and Mutual Funds are no different.

Some of the common mistakes while investing in Mutual Funds are:

- Investing without understanding the product: For example, equity funds are meant for the long term, but investors look for easy returns in the short term.

- Investing without knowing the risk factors: All Mutual Fund schemes have certain risk factors. Investors need to understand them before making an investment.

- Not investing the right amount: Sometimes people invest randomly, often without a goal or plan. In such cases, the amount invested may not yield the desired result.

- Redeeming too early: Investors sometimes lose patience or do not give the requisite time for an investment to provide the desired rate of return, and hence redeem prematurely.

- Joining the herd: Very often, investors do not exercise individual judgment and get carried away by the buzz in the ‘market’ or ‘media’, and thus make the wrong choice.

- Investing without a plan: This is perhaps the biggest mistake. Every single rupee invested needs to have a plan or goal.

# Mutual Funds vs Shares: What’s the difference?

From where do you get vegetables for dinner? Do you grow them in your backyard, or purchase it from the nearest mandi/supermarket depending on what you need? Growing your own veggies is a great way of eating healthy food, but the effort is spent on seed selection, manuring, watering, pest control, etc. The latter option allows you to choose from a wide variety without hard work.

Similarly, you can create wealth by investing directly in shares of good companies or investing in them through Mutual Funds. Wealth can be created when we buy company stocks that use our money to grow their business, creating value for us.

Direct investment in shares carries a relatively higher risk element. You need to pick stocks by researching the company and sector. It’s a humongous task to choose a few companies from thousands of them listed on the stock exchange. Once done, you need to keep track of every stock's performance.

In Mutual Funds, the stock picking is done by expert fund managers. You need to keep track of the performance of the fund and not individual stocks within the fund. They also allow investment flexibility, unlike stocks, with growth/dividend options, top-ups, systematic withdrawals/transfers, etc. besides helping to ride over volatility by investing smaller amounts regularly through SIPs.

# What is the role of an investment advisor or a Mutual Fund distributor in selecting a scheme?

# What is the role of an investment advisor or a Mutual Fund distributor in selecting a scheme?

Usually, when people select a scheme themselves, they do so based on its performance. They don’t consider that past performances may not be sustained. Evaluation of schemes is a function of various attributes of the schemes, e.g. scheme objective, investment universe, the risks that the fund is taking, etc. This requires the investor to put in time and effort. The investor also needs to have the requisite expertise to be able to understand the features and nuances as well as the ability to analyze and compare from among many options. A distributor of mutual funds or an investment advisor would be qualified and trained for such a job.

Secondly, more important than investing in the best scheme, it’s important to invest in a scheme most appropriate or suitable to the investor’s current situation. Though the investor’s situation is best known to the investor, a good advisor or distributor would be able to ask the right questions and put things in perspective.

Once the portfolio is constructed, regular monitoring of the scheme characteristics and portfolio is required, which is an ongoing job. An advisor/distributor helps you review these schemes too.

# What is the correlation between risk and return?

In Mutual Funds, one often hears, ‘more the risk, more the return’. Is there truth in this?

If ‘risk’ is measured as either, the probability of loss of capital or as swings and fluctuations in investment value, then asset classes like equity are undoubtedly the riskiest, and money in a savings bank account or in a government bond is of course least risky.

In the Mutual Fund universe, a liquid fund is the least risky and an equity fund is the most risky.

So, the only reason to invest in equity would be an expectation of a higher reward. However, higher returns come to those who invest in equity after careful study and adopting a patient, long-term time horizon. In fact, risk in equity can be mitigated by adopting diversification as well as having a longer-term time horizon.

Every category of mutual fund scheme has different types of risks – credit risk, interest rate risk, liquidity risk, market/price risk, business risk, event risk, regulatory risk, etc. The knowledge of financial experts like your mutual fund distributor/investment advisor and the fund manager, along with diversification, can help mitigate them.

# Do I need to understand stock, bond, or money markets before I invest?

Imagine you have to fly to a country far away and a plane is the only choice.

Under what circumstances do you need to understand the various controls for flying the plane? Or the various signals that the pilot receives from the different control towers? Or how to operate the radio system?

Not unless you’re a pilot or co-pilot. If you are just a passenger, you only need to understand whether your need is being served, and for that, you need to understand what you need in the first place.

In the context of investing, when you are managing your investments yourself, you need to understand the stock, bond, and money markets. However, if you decide to use Mutual Funds for the purpose of investing to reach your financial goals, you need not understand how stocks, bonds, and money markets work. You only need to know what kind of Mutual Funds serve various purposes.

Use Mutual Fund Distributor / Advisor and let an expert fund management team take over the various controls of the vehicle. You just select the vehicle based on your journey and relax.

# What kind of returns should one expect from Mutual Funds?

Imagine asking: At what speed do vehicles run?

Can you generalize the answer for the whole category? Different vehicles run at different speeds – even within one category, e.g. cars, while a car made for city roads may run at a certain maximum speed, the one made for racing can run much faster.

There is not one product called Mutual Fund, there are many types of different Mutual Funds. The investment returns from the different categories could vary and then there are certain fund categories that exhibit a higher level of uncertainty in performance.

If the fund invests in a market where prices fluctuate a lot, the Net Asset Value (NAV) of the fund is likely to witness huge fluctuations (e.g. growth funds investing in an equity market); however, if it invests in a market where prices do not fluctuate much, the Net Asset Value (NAV) of the fund would be quite stable (e.g. liquid funds investing in money market). In other terms, a liquid fund would exhibit far lower uncertainty in comparison to an equity fund.

An investor would be advised to focus on the characteristic nature of the fund and match the same with one’s own requirements.

# Are Mutual Funds suitable for those who don’t want to invest in the share market?

Some people like to play safe and opt for familiar options. Suppose you are in a new restaurant. The menu has exotic dishes, but you still order something familiar just to be sure you won’t regret it later. You may choose a regular ‘Paneer Kathi Roll’ over a ‘Couscous Paneer Salad’ to be safe. But you managed to get an idea about the new restaurant while enjoying its services, ambiance, and food.

Investing in Mutual Funds is like ordering the right dish on the menu at a restaurant. If you prefer to stay away from the stock market, you can still choose to invest in debt funds for your financial goals. Mutual Funds are broadly categorized into equity, debt, hybrid, Solution Oriented Schemes, and Other Schemes based on where they invest.

If you don’t want to invest in stocks via equity mutual funds, you can still experience the benefits of investing in mutual funds through debt funds that invest in bonds issued by banks, corporates, govt. bodies including RBI and money market instruments like commercial papers, bank CDs, T-bills, etc. A debt fund helps you grow your money better because of tax-efficient returns than your traditional choices of bank FDs, PPFs, and post office saving schemes.

# Do Mutual Funds invest only in stocks?

# Do Mutual Funds invest only in stocks?

Do you visualize roller coasters or toy trains first when you think of an amusement park? Probably the former. These rides are usually the biggest attractions in such parks which creates a certain perception about amusement parks. ‘Mutual funds’ too carry a similar perception that they invest only in stocks and hence are risky. There are many types of Mutual Funds meant for the varying investment needs of people. Some investors want high returns which only stocks can deliver. Such investors can invest in Equity Mutual Funds which are among the best long-term investment options available for achieving such objectives. But these Mutual Funds have the risk of higher volatility because of their exposure to stocks of various companies.

There are other types of Mutual Funds that do not invest in equity but in bonds issued by banks, companies, government bodies, and money market instruments (bank CDs, T-bills, Commercial Papers,) which have a lower risk but also offer lower returns compared to equity funds. These funds are better suited as alternatives to traditional options like bank fixed deposits or PPFs. Hence if you are looking to invest your money that can give you better returns than a bank or post office FDs and still be more tax efficient, Debt Mutual Funds are a great way to achieve such financial goals.

# How do I know which fund is right for me?

Once an investor has decided to invest in Mutual Funds, he has to make a decision of which scheme to invest in– Fixed Income Fund, Equity Fund, or Balanced and which Asset Management Company (AMC) to invest with.

First, discuss freely with a mutual fund distributor/investment advisor what your objective is, what time period you’re comfortable with, and what your risk appetite is.

Decisions on which fund to invest in would be made based on this information.

-

If you have a long-term objective – say, retirement planning, and are willing to assume some risk, then an Equity or Balanced Fund would be ideal.

-

If you have a very short-term objective – say, money to be kept aside for a couple of months; a Liquid Fund would be ideal.

-

If the idea is to generate regular income, then a Monthly Income Plan or an Income Fund would be recommended.

After deciding on the type of fund to invest in, a decision on the specific scheme from an AMC would have to be made. These decisions are usually made after ascertaining the AMC’s track record, suitability of the scheme, portfolio details, etc.

Scheme Factsheets and Key Information Memorandum are two documents that every investor needs to peruse before investing. If one needs detailed information then one should look at the Scheme Information Document. All of these are easily accessible on every Mutual Fund’s website.

# Does long-term mean less risk?

Investments in Mutual Funds require the appropriate time horizon. Having the right time horizon not only provides a better chance of getting the expected investment returns but also lowers the risk of the investment.

Investments in Mutual Funds require the appropriate time horizon. Having the right time horizon not only provides a better chance of getting the expected investment returns but also lowers the risk of the investment.

Now what is this “risk” we are talking about? In simple terms, it is the volatility of investment performance, as well as the chances of eroding investment capital. By staying invested over the long term, some years of low/negative returns and some years of impressive returns will make the average returns quite reasonable. Therefore, the investor can ‘average out every year’s widely fluctuating returns’ to get a more stable long-term return.

The recommended time horizon differs for every asset class as well as the Mutual Fund category. Please consult a financial expert and read the scheme-related documents before making an investment decision.

# What is the benefit of staying invested in the long term?

Invest for the long term – advice routinely given by many Mutual Fund distributors and investment advisors. This is especially true in the case of certain Mutual Funds – such as equity and balanced funds.

Let us understand why professionals give such advice. What really happens in the long term? Is there a benefit of staying invested for the long term?

Consider your Mutual Fund investment as a good quality batsman. Every good quality batsman has a certain style of batting. However, each good quality batsman would be able to accumulate lots of runs, if he continues to play for years.

We are talking about the record of a “good quality” batsman. Every good batsman would go through some good and poor performances. On average the record would be impressive.

Similarly, a good Mutual Fund would also go through some ups and downs – often due to factors beyond the control of the fund manager. An investor would benefit if one stays invested through these funds for long periods of time.

So, as long as you can afford, stay invested for long periods of time – especially in equity and balanced funds.

# How to deal with rumors while investing?

How often have you come across people you know who have lost money in the stock market because they couldn’t guess where the market would go next moment or who made money because they knew where the market was headed next? Even the best market analysts can’t predict with absolute precision how the market will move the very next moment because financial markets are driven by sentiments and market sentiments are driven by market news.

An investor today has easy access to market news that may be factually correct or could be a rumor or mere speculation. While investment decisions based on factually correct news may yield positive results, investment decisions based on rumors or speculations can cause losses to investors.

According to Behavioral Finance Theory, investors are irrational by nature i.e. their investment behavior is not backed by thorough research and analysis but rather influenced by various cognitive and emotional biases including herd mentality. Hence, any incorrect market information can fuel panic amongst investors leading to huge erosion of investor wealth.

Then how can an investor hold himself steady when the market is flooded with all kinds of news ranging from verified ones to rumors? This is where Mutual Fund investments can come to the rescue of millions of small investors who lack the capability and resources to carry out extensive research and analysis. Investing in mutual funds helps circumvent all the above problems as professional fund managers take care of the investment decisions on your behalf. Also, mutual fund investments held over a long period of time help you tide over short-term fluctuations caused by market volatility that is many times fueled by market rumors.

Fund managers have a team of research analysts who carry out extensive research based on all public information to evaluate each security before taking a decision to buy, hold or sell it. You can always reach out to your SEBI registered financial advisor or mutual fund distributor for guidance in case you come across some market news regarding any security in the fund’s portfolio or about the fund that sounds worrisome.

# What happens when the market falls midway while you have invested for a longer term?

Mutual Fund investors with long-term investments through SIPs constantly worry about market falls during this period. SIPs are well-designed to overcome some of the Mutual Fund risks like market timing and volatility.

Mutual Fund investors with long-term investments through SIPs constantly worry about market falls during this period. SIPs are well-designed to overcome some of the Mutual Fund risks like market timing and volatility.

You can beat market volatility through rupee-cost averaging, by investing regularly in Mutual Funds through SIPs. Here you buy more units when NAV is low and vice versa. The cost per unit is averaged out over the long run if NAVs move both ways. For example, if you invest INR 1,000/- per month, you get 100 units if the NAV is INR 10 and 200 units if NAV drops to INR 5. Over the longer-time period, the average price per unit will fall if markets move in both directions thus helping to lower the volatility of returns as well.

If you invest in a lump sum, the number of units would remain the same during the entire holding period, but their value would go down with falling NAV during market downturns. If you hold your lumpsum investment in an equity fund for a long (say over 7-8 years), the occasional blips shouldn’t impact your returns as markets usually move up over the long term. You might end up with a far higher NAV than what you started with.

# When should I start investing in Mutual Funds?

There is a beautiful Chinese proverb, “The best time to plant a tree was 20 years ago. The second-best time is now.”

There is no reason why one should delay one’s investments, except, of course, when there is no money to invest. Within that, it is always better to use Mutual Funds than to do it oneself.

There is no minimum age when one can start investing. The moment one starts earning and saving, one can start investing in Mutual Funds. In fact, even kids can open their investment accounts with Mutual Funds out of the money they receive once in a while in the form of gifts during their birthdays or festivals. Similarly, there is no upper age for investing in Mutual Funds.

Mutual Funds have many different schemes suitable for different purposes. Some are suitable for growth over long periods, whereas some may be for those in need of safety with regular income, and some provide liquidity in the short term, too.

You see, whatever stage of life one is in, or whatever one’s requirements, Mutual Funds may have solutions for each one.

# How can I track my investments on a regular basis?

Investors often wonder how to go about tracking the progress of their investments.

It is like chasing a target in a cricket match. In a cricket match, the team batting second knows the equation – how many runs, how many wickets and how many overs.

It is like chasing a target in a cricket match. In a cricket match, the team batting second knows the equation – how many runs, how many wickets and how many overs.

It is very similar when it comes to investing for the achievement of financial goals, too. Consider the financial goal as the target score-

- The amount you have accumulated so far is the runs you have scored so far.

- The amount yet to be accumulated is the runs to be scored and the time left is the overs left.

- The condition of the wickets and the quality of the bowlers may be compared to various risks – be it related to the national or global economy; global capital flows; political situation in the country; changes in laws, regulations, and taxes, etc.

- The scoreboard in this case is the account statement you get when you invest in a Mutual Fund scheme.

- There are also online tools, and mobile apps available to check the value of one’s investments – the scoreboard.

# Won’t I need a large amount to invest in Mutual Funds?

People think that Mutual Funds are elite investments made only for the wealthy. The fact is: that one does not need a large sum to invest in Mutual Funds, you can start with a sum as low as ₹ 500, or 5000 depending on the kind of fund you choose.

Why keep the minimum amounts as low as these?

The economies of scale can be understood easily if we look at traveling by airplane. The plane would cost a lot of money and, of course, not everybody owns a plane! However, we can afford air travel simply because all the costs are divided among all the passengers using the services at various different points of time.

Similarly, a person may not have enough money to create a diversified portfolio through investment in a very large number of investment avenues, one may not have enough money required to conduct or purchase research on investments. However, the economies of scale allow small investors to get multiple benefits through Mutual Funds.

Mutual Funds are thus ideal vehicles for small investors for saving and investing.

# Cost of delay/impact of compounding in Mutual Funds:

When you invest in a mutual fund over a long period of time, the returns you earn have a compounding effect. However, if you delay your investments by a few years, you’ll lose out on the same. This compounding effect will widen the difference between what you will accumulate versus what you could have accumulated had you started investing a few years earlier.

The compounding effect shows its magic over the long term because the longer you stay invested, the more time your money gets to compound. The power of compounding is like a magnifying glass whose magnifying power grows exponentially over time. If you delay your investments, whether through SIP or in lumpsum and invest a higher amount, you will still not be able to catch up with someone who started investing say five years before you. In the case of a SIP he/she may be investing half the amount you are investing but your investments will still lag behind. Even with a lumpsum investment, a delay of a few years would mean your accumulated wealth will be less than someone who invested in a lumpsum a few years before you. That’s a huge cost to pay for delaying your investment decision.

If you start investing early in Mutual Funds, even if your investment amount is small, you are likely to accumulate much higher wealth over a few decades compared to if you start investing a higher amount by say 10 years later. It’s just like the hare and the tortoise story wherein slow and steady investments initiated early in life will help you reach your goal comfortably instead of starting late even though you are willing to invest more.

# At what age should one start investing?

# At what age should one start investing?

you are wondering if is it too early or late to invest in Mutual Funds, rest assured that the right age to start investing is in fact now, the moment you decide to invest. But the sooner you start investing, the better will it be for you since mutual funds help in creating wealth over the long term through the power of compounding.

For the power of compounding to work its magic on your investments, you must start early in your career. In fact, the ideal time to get into Mutual Funds would be the day you start earning. If you can save a little from your monthly earnings and invest it in Mutual Funds through SIP, you are giving your money a long enough time to grow. You’ll be able to reap the benefits of such a disciplined investment approach in the future when the need arises. Remember to invest in those mutual fund schemes with risk levels that match your risk appetite i.e. your ability and willingness to take that kind of risk.

As we progress through life, our life goals grow bigger with growing salaries. Start your investment journey through a SIP with your first salary and increase it with every pay hike in order to meet these goals comfortably. But even if you haven’t started yet, it is never too late to start your Mutual Fund journey today because the power of compounding can still give you something more than if you delay the decision by a few years from now.

# How do I start/stop a SIP? What happens if I miss an installment?

Before you make any Mutual Fund investment, you need to complete a KYC process. This is done through the submission of certain documents as proof of identity and proof of address. The process of starting or stopping a SIP is extremely convenient and easy. How to start a SIP is explained in the graphics on the left.

What happens when you skip an installment or two?

SIP is just a convenient mode of investing and not a contractual obligation, there is no penalty even if you miss an installment or two. At most, the Mutual Fund Company would stop the SIP, which means further installments would not get debited from your bank account. At the same time, you can always start another SIP, even in the same folio, even after the earlier SIP was stopped. Please keep in mind, this would be treated as a fresh SIP and hence there could be some time taken to set up the SIP all over again.

Consult with a financial expert today and start enjoying the benefits of Mutual Funds!

# Why continue investing through SIPs in a volatile market?

When the markets turn volatile many investors start doubting their investment decisions and think of stopping their SIPs or withdrawing their investments. It’s natural to get worried when you see your investments in the red during a volatile market. But it would be wise to stay put with your SIPs, especially during a falling market because, with the same amount of monthly investments, you will end up buying more units. We all love to bargain shopping be it during an online sale or simply at the sabzi shop. Isn’t it? Then why not for our Mutual Fund investments when prices are falling?

When the markets turn volatile many investors start doubting their investment decisions and think of stopping their SIPs or withdrawing their investments. It’s natural to get worried when you see your investments in the red during a volatile market. But it would be wise to stay put with your SIPs, especially during a falling market because, with the same amount of monthly investments, you will end up buying more units. We all love to bargain shopping be it during an online sale or simply at the sabzi shop. Isn’t it? Then why not for our Mutual Fund investments when prices are falling?

The market is more unpredictable than even our weather forecast apps. You can never time yourself perfectly to invest a lumpsum amount when the market falls. What if the market falls further after you’ve invested? Similarly, you cannot time yourself perfectly to sell at a market high because the market may go up further after you’ve sold. If you try to catch the market, you will be grossly disappointed, and your returns can be affected due to the wrong timing. Hence it is better to invest regularly through the highs and lows of the market by investing through a SIP with a clear focus on your goals. You need not worry about market volatility since the cost of your investments will average over a period.

# Why should one not be bothered by volatility in mutual funds?

During a long drive, do you worry about your speed or the destination and how to get there? Obviously, you don’t count the bumps but focus on reaching your destination safely in time. The same goes with Mutual Funds. You shouldn’t worry about the daily NAV fluctuations but rather focus on whether it is taking you closer to the financial goal in the time you have set for it.

During the drive, there are numerous times when your speed drops to near zero, but the vehicle picks up speed once you get over the bump and continue your journey. At the end of the trip, what matters is the average speed you clocked to reach your destination. Similarly, a mutual fund can have numerous bumps in the short term but the longer you stay invested, the impact of these fluctuations decreases and your chances of earning a positive return go up just like your car’s average speed during a long trip.

Every economy and hence market goes through periods of growth and recession which impact on your fund’s return but only in the short term. Over the long term, your fund would have gone through several such bouts of ups and downs, but their impact would be muted because it’s the long-term compounded total return that will count at the end of your investment journey.

# Is mutual fund investment a plan for every goal?

Yes, Mutual Funds are ideal to help you plan your life goals!

- Mr. Rajput eventually wants to move away from the city, into a farmhouse on a hill station when he plans to retire after 15-20 years.

- Mrs. Patel didn’t receive any retirement benefits. Although she has savings, she now needs a regular income from her investments to meet her regular expenses.

- Mrs. Sharma has surplus money generated from her business and lets it lie idle in her bank account. She is required to pay her suppliers and staff only after a few days.

The above could be real-life situations. Is there any option available for these investors?

YES! Mutual Funds!

Mutual Funds offer different kinds of schemes for different kinds of investment objectives. For e.g.

- Long-term goals like building a corpus for retirement – You could consider equity and balanced funds

- Looking to generate income with relatively low risk – You could consider a bond fund

- Park your surplus money till you decide where to invest it next – You could consider a liquid fund

Mutual Funds offer different kinds of investment options for planning one’s investments, especially when one is clear about their goals.

# Are there penalties if I choose to withdraw earlier?

Every open-ended scheme offers liquidity with almost complete freedom, i.e. no restriction on time or amount of redemption. However, a few schemes may specify an Exit Load.

For example, a scheme specifies an exit load of 1%, if redeemed within 1 year. What it means is that, if an investor has invested on April 1, 2016, any redemption done on or before March 31, 2017, would attract a penalty of 1% on the NAV. If an investor redeems on February 1, 2017, with the NAV at ₹ 200, then ₹ 2 would be deducted and only ₹ 198 per unit would be returned to the investor.

All information on exit loads is usually mentioned in relevant scheme-related documents. For instance, a fund fact sheet or key information memorandum would contain such information.

Mutual Fund- SIP

# What is Systematic Investment Plan (SIP)?

A systematic Investment Plan (SIP) is an investment route offered by Mutual Funds wherein one can invest a fixed amount in a mutual fund scheme at regular intervals– say once a month or once a quarter, instead of

making a lump-sum investment. The installment amount could be as little as INR 500 a month and is similar to a recurring deposit. It’s convenient as you can give your bank standing instructions to debit the amount every month.

making a lump-sum investment. The installment amount could be as little as INR 500 a month and is similar to a recurring deposit. It’s convenient as you can give your bank standing instructions to debit the amount every month.

SIP has been gaining popularity among Indian MF investors, as it helps in investing in a disciplined manner without worrying about market volatility and timing the market. Systematic Investment Plans offered by Mutual Funds are easily the best way to enter the world of investments for the long term. It is very important to invest for the long term, which means that you should start investing early, in order to maximize the end returns. So, your mantra should be - Start Early, Invest Regularly to get the best out of your investments.

# SIP কি?

এসআইপি মানে সিস্টেমেটিক ইনভেস্টমেন্ট প্ল্যান। একটি বিনিয়োগের বিকল্প যা আপনাকে নিয়মিত এবং সুশৃঙ্খলভাবে অল্প পরিমাণে বিনিয়োগ করতে দেয়। এই সব আপনার মাসিক বাজেট ব্যাহত ছাড়া.

# কেন একটি SIP শুরু করবেন?

এটি আপনার বড় জীবনের স্বপ্নগুলিকে ছোট, আরও অর্জনযোগ্য লক্ষ্যে বিভক্ত করে আপনার আর্থিক লক্ষ্যগুলি অর্জনের একটি কার্যকর পদ্ধতি।

# কিভাবে একটি SIP শুরু করবেন?

SIP এর মাধ্যমে আপনার সঞ্চয় স্বয়ংক্রিয় করা একটি সহজ 4-পদক্ষেপ প্রক্রিয়া।

- আপনার বিনিয়োগের পরিমাণ নির্ধারণ করুন।

- আপনার বিনিয়োগ ফ্রিকোয়েন্সি নির্বাচন করুন.

- একটি শুরুর তারিখ সেট করুন।

- আপনার এসআইপি বিনিয়োগের জন্য একটি মিউচুয়াল ফান্ড বেছে নিন।

সেট আপ সম্পূর্ণ হলে, প্রক্রিয়া স্বয়ংক্রিয়ভাবে সঞ্চালিত হয়.

# আমি একটি SIP বিনিয়োগে কত রিটার্ন আশা করতে পারি?

# আমি একটি SIP বিনিয়োগে কত রিটার্ন আশা করতে পারি?

প্রচলিত স্থির আয়ের পণ্যের বিপরীতে, মিউচুয়াল ফান্ড বিনিয়োগ একটি গ্যারান্টিযুক্ত রিটার্ন প্রদান করে না। কিন্তু, ঐতিহাসিকভাবে, দীর্ঘ মেয়াদে, ইক্যুইটি ফান্ডে বিনিয়োগ ঐতিহ্যগত স্থির-আয় পণ্যের তুলনায় ভালো রিটার্ন তৈরি করেছে। বলা হয়েছে, মিউচুয়াল ফান্ড বিনিয়োগ বাজারের ঝুঁকির বিষয়। বিনিয়োগ করার আগে আপনাকে সমস্ত স্কিম-সম্পর্কিত নথি সাবধানে পড়ার পরামর্শ দেওয়া হচ্ছে।

# সেরা কিছু SIP প্ল্যান কি কি?

"সেরা মিউচুয়াল ফান্ড" বলে কিছু নেই। এটা একটা মিথ। প্রতিটি তহবিলের একটি অনন্য বিনিয়োগ উদ্দেশ্য থাকে যা বিভিন্ন বিনিয়োগকারীদের চাহিদা পূরণ করে। আপনার ঝুঁকির ক্ষুধা এবং আপনার জীবনের লক্ষ্য অর্জনের সময়সীমার উপর ভিত্তি করে আপনাকে নিজের জন্য সঠিক তহবিল নির্বাচন করতে হবে।

# "এসআইপি ফ্রিকোয়েন্সি" বলতে কী বোঝায়?

এসআইপি ফ্রিকোয়েন্সি বলতে পূর্ব-নির্ধারিত ব্যবধানকে বোঝায় যেখানে একটি নির্দিষ্ট পরিমাণ, আপনার দ্বারা বাধ্যতামূলক, আপনার ব্যাঙ্ক অ্যাকাউন্ট থেকে কেটে নেওয়া হয়। আপনি একটি মাসিক, ত্রৈমাসিক, আধা-বার্ষিক বা বার্ষিক ফ্রিকোয়েন্সি সহ যেতে পারেন।

# একটি SIP শুরু করার জন্য কি ন্যূনতম পরিমাণ আছে?

একটি S.I.P শুরু করার জন্য সর্বনিম্ন পরিমাণ ফান্ড থেকে ফান্ডে পরিবর্তিত হয়। এটা বলার পরে, ভারতে অনেক তহবিল এখন আপনাকে একটি S.I.P শুরু করতে দেয়। 500 টাকা। S.I.P এর মাধ্যমে বিনিয়োগ অল্প পরিমাণে সীমাবদ্ধ নয়। আপনি চাইলে যেকোন পরিমাণ বিনিয়োগ করতে পারেন। S.I.P এর কোন ঊর্ধ্বসীমা নেই SIP এর ন্যূনতম মেয়াদ 6 মাস, যেখানে সর্বোচ্চ কোন মেয়াদ নেই।

# আপনি মিউচুয়াল ফান্ডগুলিতে শুধুমাত্র ₹ 500 টাকা প্রতি মাসে দিয়ে বিনিয়োগ শুরু করতে পারেন!

লোকজনা মনে করেন যে অর্থপূর্ণ আয় ফেরত পাওয়ার জন্য, বেশি পরিমাণ অর্থ মিউচুয়াল ফান্ডগুলিতে বিনিয়োগ করতে হয়। আপনি বিনিয়োগ সামান্য থেকে সামান্য যেমন ধরুন ₹ 500 টাকা প্রতি মাসে শুরু করুন এবং ধীরে ধীরে বিনিয়োগ বাড়ান আপনার আয় বৃদ্ধি হওয়ার সাথে সাথে।

# রিটার্ন বা ফেরতের বিভিন্ন হারে আপনার বিনিয়োগগুলি কিভাবে বাড়তে পারে তা বুঝতে নিচের টেবিলটি দেখুন।

*এটি স্থায়ীভাবে একটি উদাহরণ। টেবিলে দেখানো রিটার্নগুলি কেবলমাত্র কাল্পনিক এবং চিত্রণের উদ্দেশ্যে ব্যবহৃত। মিউচুয়াল ফান্ডে রিটার্নের কোনও সুনিশ্চিত হার প্রস্তাব করে না।

মিউচুয়াল ফান্ডগুলি সাধারণ মানুষ থেকে বড় লোক (একজন সাধারণ মানুষ থেকে উচ্চ মোট মূল্যের স্বতন্ত্র ব্যক্তি) পর্যন্ত প্রত্যেকের জন্য। একটি বড় উদ্দেশ্যের জন্য ছোট সংরক্ষকের লক্ষ্যের সহায়তা করার জন্য তিনটি মন্ত্র রয়েছে:

ক. তাড়াতাড়ি শুরু করুন এমনকি ছোট পরিমাণ দিয়েও

খ. নিয়মিত বিনিয়োগ করুন সে যতোই কম পরিমাণ হোক না কেন

গ. দীর্ঘ মেয়াদের জন্য বিনিয়োগ করে রাখুন-আপনার বিনিয়োগকে বৃদ্ধি হওয়ার সুযোগ করে দেওয়ার জন্য

মিউচুয়াল ফান্ড সময়ের সঙ্গে সব রকমের বিনিয়োগকারীর জন্য বিকশিত হয়েছে। এমনকি যদি বিনিয়োগের পরিমাণ কম হলেও, নিয়মিত বিনিয়োগগুলি এবং একটি শৃঙ্খলাবদ্ধ পদ্ধতি আপনাকে সময়ের সাথে বড় সংস্থান গড়ে তুলতে সহায়তা করতে পারে।

# SIP এর মাধ্যমে আমি সর্বোচ্চ কত টাকা বিনিয়োগ করতে পারি?

S.I.P এর মাধ্যমে বিনিয়োগ অল্প পরিমাণে সীমাবদ্ধ নয়। আপনি চাইলে যেকোন পরিমাণ বিনিয়োগ করতে পারেন। S.I.P এর কোন ঊর্ধ্বসীমা নেই

# আমি কি একাধিক SIP পেতে পারি?

হ্যাঁ, আপনি একাধিক S.I.P শুরু করতে পারেন। একটি নির্দিষ্ট সময়ে আপনার কতগুলি সিস্টেমেটিক ইনভেস্টমেন্ট প্ল্যান থাকতে পারে তার উপর কোন সীমাবদ্ধতা নেই।

# "রুপি খরচ গড়" বলতে কী বোঝায়?

S.I.P এর অন্যতম প্রধান সুবিধা হল রুপি কস্ট এভারেজিং। এর সহজ অর্থ হল যে আপনি যখন বাজার কমতে থাকে তখন আপনি বেশি ইউনিট পাবেন এবং যখন বাজার উপরে যায় তখন কম পাবেন। এইভাবে, আপনি কেনা মোট ইউনিটের খরচ গড়। এটি আপনাকে দীর্ঘ মেয়াদে রিটার্ন অপ্টিমাইজ করতে সহায়তা করে।

# আমি কি যেকোন সময় SIP এর পরিমাণ পরিবর্তন করতে পারি?

# আমি কি যেকোন সময় SIP এর পরিমাণ পরিবর্তন করতে পারি?

হ্যাঁ, আপনি আপনার S.I.P বাড়াতে পারেন। যে কোনো সময়ে পরিমাণ। এটি করার দুটি উপায় আছে। আপনি হয় একটি নতুন S.I.P শুরু করতে পারেন অতিরিক্ত পরিমাণের সাথে অথবা আপনি একটি সুবিধা বেছে নিতে পারেন, যা সাধারণত S.I.P নামে পরিচিত। বুস্টার বা S.I.P. টপ-আপ, যা আপনাকে আপনার S.I.P বাড়াতে দেয়। একটি পূর্ব-নির্ধারিত ব্যবধানে কিস্তির পরিমাণ।

# আমি কি যেকোনো সময় আমার SIP বন্ধ করতে পারি?

হ্যাঁ, আপনি যেকোনো সময়ে আপনার SIP কিস্তি বন্ধ করতে পারেন। একটি S.I.P বন্ধ করার জন্য কোন চার্জ নেওয়া হয় না তাছাড়া, আপনি আগের কিস্তির মাধ্যমে জমাকৃত করপাস উত্তোলন করতে পারেন।

# আমার SIP কিস্তি যদি অপর্যাপ্ত অ্যাকাউন্ট ব্যালেন্সের কারণে পূরণ করতে ব্যর্থ হয় তাহলে আমি কি শাস্তি পেতে পারি?

আপনার অ্যাকাউন্টের ব্যালেন্স অপর্যাপ্ত হলে S.I.P. কিস্তি বকেয়া আছে। এটা ঠিক যে সেই নির্দিষ্ট মাসের জন্য আপনার কিস্তি প্রক্রিয়া করা হবে না, কিন্তু আপনার S.I.P. পরের মাস থেকে স্বাভাবিকভাবে চলতে থাকবে, যদি ব্যালেন্স যথেষ্ট থাকে।

# একটি SIP এর জন্য আদর্শ বিনিয়োগ দিগন্ত কি?

এসআইপি দীর্ঘমেয়াদে সম্পদ তৈরির লক্ষ্যে নিয়মিত একটি নির্দিষ্ট পরিমাণ সঞ্চয় ও বিনিয়োগ করার একটি ভাল অভ্যাস। তাই, একজন S.I.P. চিরকালের জন্য করা উচিত, যদি না আপনি একটি S.I.P শুরু করছেন। একটি নির্দিষ্ট লক্ষ্যের জন্য যা একটি নির্দিষ্ট তারিখে প্রযোজ্য।

# কোন SIP ফ্রিকোয়েন্সি ভাল - সাপ্তাহিক বা মাসিক?

একই হারের রিটার্ন ধরে নিলে, একটি সাপ্তাহিক ফ্রিকোয়েন্সি একটি ভাল পছন্দ হিসাবে পরিণত হবে কারণ আপনি চক্রবৃদ্ধির সুবিধা পাবেন। দুর্ভাগ্যবশত, বাজারের রিটার্ন অনুমানযোগ্য নয়। অতএব, কোন ফ্রিকোয়েন্সি ভাল তার কোন সঠিক উত্তর নেই। বলা হচ্ছে, আপনার নগদ প্রবাহের উপর ভিত্তি করে ফ্রিকোয়েন্সি নির্বাচন করার পরামর্শ দেওয়া হচ্ছে। তাই, বেতনভোগী ব্যক্তিরা তাদের S.I.P এর জন্য মাসিক ফ্রিকোয়েন্সি পছন্দ করেন।

# কোন অতিরিক্ত বা লুকানো খরচ আছে যা আমি একটি SIP শুরু করার জন্য বহন করব?

না, S.I.P শুরু করার জন্য কোন অতিরিক্ত চার্জ বা লুকানো খরচ নেই।

# যদি আমার বিনিয়োগে রিটার্ন নেতিবাচক হয়, তাহলে আমার কী করা উচিত?

নেতিবাচক রিটার্নের মুখোমুখি হওয়ার সময়, বিনিয়োগকারীরা সবচেয়ে সাধারণ ভুলটি করে থাকে তাদের S.I.P বন্ধ করা। এবং জমে থাকা কর্পাস প্রত্যাহার করুন। আদর্শভাবে, আপনার যদি দীর্ঘমেয়াদী বিনিয়োগের দিগন্ত থাকে, তাহলে বাজারের মন্দাকে মোট ইউনিটের খরচ গড় করার জন্য আরও বেশি কেনার সুযোগ হিসাবে বিবেচনা করা উচিত। বাজার ইতিবাচক হয়ে উঠলে এটি আপনাকে অনুকূল রিটার্ন জেনারেট করতে সাহায্য করবে।

# "SIP বুস্টার" বা "SIP টপ-আপ" বলতে কী বোঝায়?

S.I.P বুস্টার বা S.I.P টপ-আপ আপনাকে পূর্ব-নির্ধারিত ব্যবধানে আপনার S.I.P কিস্তির পরিমাণ বাড়াতে দেয়। এইভাবে, আপনাকে একটি নতুন S.I.P শুরু করতে হবে না। মাঝে মাঝে. কিস্তির পরিমাণ বৃদ্ধি একটি নির্দিষ্ট অর্থ হতে পারে বা এটি আপনার বর্তমান কিস্তির মূল্যের শতাংশ হতে পারে।

# যদি একই বিভাগের বিভিন্ন মিউচুয়াল ফান্ডের স্কিম পাওয়া যায়, তাহলে কি কম NAV সহ একটি স্কিম বেছে নেওয়া উচিত?

অনুমান করে আপনি অভিন্ন পোর্টফোলিও সহ দুটি ভিন্ন ফান্ডে ঠিক একই পরিমাণ বিনিয়োগ করেন, একটি কম NAV তহবিল আপনাকে অনেক বেশি ইউনিট আনবে, যেখানে একটি উচ্চ NAV তহবিল আপনাকে কম সংখ্যক ইউনিট আনবে। রিটার্নগুলি বিনিয়োগের মূল্য দ্বারা নির্ধারিত হয় এবং পোর্টফোলিওতে স্টকগুলির মূল্যায়ন বা অবমূল্যায়নের একটি ফ্যাক্টর, ইউনিটের সংখ্যা নয়। অতএব, NAV অর্থহীন।

# কোনটি ভালো - লাম্পসাম নাকি এসআইপি?

এই প্রশ্নের উত্তর নির্ভর করে শেয়ার বাজারের অবস্থার উপর। ঊর্ধ্বমুখী প্রবণতার সময়, মিউচুয়াল ফান্ড বিনিয়োগের একমুঠো মোড তুলনামূলকভাবে বেশি রিটার্ন দেয় যেখানে পতনশীল বাজারের সময়, একটি SIP-এর মাধ্যমে করা বিনিয়োগ সাধারণত একমুঠো বিনিয়োগের চেয়ে ভাল রিটার্ন প্রদান করে। বলা হয়েছে, পছন্দ আপনার নগদ-প্রবাহের উপরও নির্ভরশীল।

# মিউচুয়াল ফান্ডে আমার বিনিয়োগ কি নিরাপদ?

মিউচুয়াল ফান্ডে ঝুঁকির মাত্রা নির্ভর করে এটি কী বিনিয়োগ করে। স্টকগুলি সাধারণত বন্ডের চেয়ে বেশি ঝুঁকিপূর্ণ, তাই একটি ইক্যুইটি ফান্ড একটি নির্দিষ্ট আয়ের তহবিলের চেয়ে ঝুঁকিপূর্ণ হতে থাকে। এছাড়াও, কিছু বিশেষ মিউচুয়াল ফান্ড উচ্চতর রিটার্ন অর্জনের চেষ্টা করার জন্য উদীয়মান বাজারের মতো নির্দিষ্ট ধরণের বিনিয়োগের উপর ফোকাস করে। এই ধরনের তহবিলগুলির মূল্য হ্রাসের একটি বৃহত্তর ঝুঁকি থাকে তবে ঝুঁকি যত বেশি, তত বেশি পুরস্কার বা উচ্চতর রিটার্নের সম্ভাবনা।

# আমি কিভাবে একটি মিউচুয়াল ফান্ড বেছে নেবো?

ধরুন একটি ট্র্যাভেল এজেন্টকে জিজ্ঞাসা করলেন, "আমি কিভাবে আমার পরিবহনের মোড নির্বাচন করব?" তিনি প্রথমেই আপনাকে বলবেন, "সেটা নির্ভর করছে আপনি কোথায় যেতে চান তার উপরে।" যদি আমি 5 কিলোমিটার দূরত্বে ভ্রমণ করতে যাই, তাহলে অটো রিক্সা সবচেয়ে ভালো উপায় হতে পারে, আর যদি নিউ দিল্লী থেকে কোচি যেতে হয়, সেক্ষেত্রে একটি ফ্লাইট নেওয়াই সবচেয়ে ভালো। কম দূরত্বের জন্য ফ্লাইট পাওয়া যায় না এবং একটি দীর্ঘ যাত্রার জন্য অটো রিক্সা ব্যবহার করা অত্যন্ত অস্বস্তিকর এবং অত্যাধিক সময়সাপেক্ষ ।

ধরুন একটি ট্র্যাভেল এজেন্টকে জিজ্ঞাসা করলেন, "আমি কিভাবে আমার পরিবহনের মোড নির্বাচন করব?" তিনি প্রথমেই আপনাকে বলবেন, "সেটা নির্ভর করছে আপনি কোথায় যেতে চান তার উপরে।" যদি আমি 5 কিলোমিটার দূরত্বে ভ্রমণ করতে যাই, তাহলে অটো রিক্সা সবচেয়ে ভালো উপায় হতে পারে, আর যদি নিউ দিল্লী থেকে কোচি যেতে হয়, সেক্ষেত্রে একটি ফ্লাইট নেওয়াই সবচেয়ে ভালো। কম দূরত্বের জন্য ফ্লাইট পাওয়া যায় না এবং একটি দীর্ঘ যাত্রার জন্য অটো রিক্সা ব্যবহার করা অত্যন্ত অস্বস্তিকর এবং অত্যাধিক সময়সাপেক্ষ ।

মিউচুয়াল ফান্ডের ক্ষেত্রেও, প্রথম পদক্ষেপটি হল - আপনার প্রয়োজনীয়তা কি?

এটি আপনার আর্থিক লক্ষ্য এবং রিস্ক অ্যাপেটাইট দিয়ে শুরু হয়।

আপনাকে প্রথমে আপনার আর্থিক লক্ষ্যগুলি চিহ্নিত করতে হবে। কিছু মিউচুয়াল ফান্ড স্কিম স্বল্পমেয়াদী প্রয়োজনীয়তা বা লক্ষ্যের জন্য উপযুক্ত, আবার কিছু কিছু স্কিম দীর্ঘমেয়াদী লক্ষ্যের জন্য আদর্শ হতে পারে।

এরপরে আসে আপনার রিস্ক অ্যাপেটাইট। বিভিন্ন ব্যক্তির রিস্ক অ্যাপেটাইট বা ঝুঁকির ক্ষুধা বিভিন্ন রকম। এমনকি স্বামী এবং স্ত্রীয়ের যৌথ আর্থিক ব্যবস্থা থাকাতে পারে কিন্তু তাদের রিস্ক প্রোফাইল আলাদা হতে পারে। অনেকে উচ্চ ঝুঁকিযুক্ত পণ্যে স্বচ্ছন্দ বোধ করেন, আবার অনেকেই তা বোধ করেন না।

আপনার ঝুঁকি নেওয়ার ক্ষমতা মূল্যায়ন করতে, আপনি বিনিয়োগ উপদেষ্টা বা মিউচুয়াল ফান্ড ডিস্ট্রিবিউটরদের মতো আর্থিক বিশেষজ্ঞদের সাহায্য নিতে পারেন।

# তাহলে ডিসক্লেইমারে কেন বলা হয় যে মিউচুয়াল ফান্ড বাজারের ঝুঁকি সাপেক্ষ?

মিউচুয়াল ফান্ডগুলি সিকিউরিটিজে বিনিয়োগ করে এবং সিকিউরিটির প্রকৃতি স্কিমের উদ্দেশ্যের উপরে নির্ভর করে।

উদাহরণস্বরূপ, একটি ইকুইটি বা গ্রোথ ফান্ড কোম্পানির শেয়ারে বিনিয়োগ করবে। একটি লিকুইড ফান্ড বিনিয়োগ করবে ডিপোসিটের সার্টিফিকেট ও বাণিজ্যিক কাগজপত্রে।

এই সকল সিকিউরিটিজগুলি যদিও বাজারে লেনদেন করা হয়। স্টক এক্সচেঞ্জের মাধ্যমে কোম্পানির শেয়ার ক্রয় ও বিক্রয় করা হয় যা ক্যাপিটাল মার্কেটের অংশ। একইভাবে, সরকারী সিকিউরিটিজের মতো ঋণ সাধনের জন্য স্টক এক্সচেঞ্জে বা NDS নামক বিশেষ ব্যবস্থার মাধ্যমে একটি প্ল্যাটফর্মের মাধ্যমে ট্রেড করা যেতে পারে। এগুলি সিকিউরিটিজ ক্রয় ও বিক্রয়ের বাজার হিসাবে পরিবেশন করে এবং বিভিন্ন ধরণের ক্রেতা ও বিক্রেতারা থাকেন। সুতরাং, কেনা এবং বিক্রি করার সম্পূর্ণ প্রক্রিয়া, এবং মূল্যনির্ধারণ 'মার্কেট' এর দ্বারা করা হয়।

যে কোনও সিকিউরিটিজের মূল্য 'মার্কেট ফোর্সেস’-এর উপর নির্ভরশীল, এবং বাজার যে কোনও খবর বা বিকাশে প্রতিক্রিয়া জানায়, যার ফলে বাজারের দিকনির্দেশের পূর্বানুমান করা কঠিন হয়ে ওঠে, যার ফলে স্বল্পমেয়াদী ক্ষেত্রে কোনও শেয়ারের মূল্য অথবা সিকিউরিটির পূর্বানুমান করা অসম্ভব। এর অভিমুখকে প্রভাবিত করার জন্য একাধিক কারণ এবং খেলোয়াড় আছে।

সুতরাং, প্রত্যেক বিনিয়োগকারীর এটি জানা উচিৎ যে সিকিউরিটি মূল্যের জন্য ‘মার্কেট’ নামক সবচেয়ে গুরুত্বপূর্ণ একটি সত্তার কাছ থেকে সর্বদা একটি নির্দিষ্ট পরিমাণ ঝুঁকি বিদ্যমান। তাদের এও জানা উচিৎ যে মিউচুয়াল ফান্ডগুলিকে যতটা সম্ভব এই ঝুঁকি হ্রাস করার জন্য ডিজাইন করা হয়েছে।

Child Education to Retirement Planning

# FINANCIAL PLANNING FOR YOUR CHILD'S FUTURE WITH MUTUAL FUND:

There is no better gift you can give your child, than the promise of a secure future. After becoming a parent, one should start planning for the child’s future by investing in comprehensive health and education plans. Before you plan to buy health insurance or a child education plan, you must consider aspects such as the premium rate, inflation rate, the cost of education, and medical.

Planning for the future financial security of a child is a challenging task. Individuals attempt to create a robust financial cushion for their children, but, at the hour of truth, find that the funds they have accumulated are not sufficient. Creating a financial backup for a child may require parents, not to invest in merely a single plan, but a few good child investment plans on the market today. The key to making investments to safeguard a child’s financial future is to make the appropriate choices of investment at the correct time. Like all investments, making plans for the future involves taking stock of each individual requirement and the financial goals that are unique to particular parents and their children.

Planning for the future financial security of a child is a challenging task. Individuals attempt to create a robust financial cushion for their children, but, at the hour of truth, find that the funds they have accumulated are not sufficient. Creating a financial backup for a child may require parents, not to invest in merely a single plan, but a few good child investment plans on the market today. The key to making investments to safeguard a child’s financial future is to make the appropriate choices of investment at the correct time. Like all investments, making plans for the future involves taking stock of each individual requirement and the financial goals that are unique to particular parents and their children.

Children are the world to parents and they strive hard to give them the best. When it comes to their education and financially securing their future, timely investments need to be the top priority. The rise in education costs makes it important to invest in your child.

If you are a parent looking for the best investment options for your kid’s future, you are at the right place. Our financial experts have identified some of the best investments for children.

Mutual Funds are quite popular among investors because of their diversification and risk management. The best part about mutual funds is that they are not just for the rich or for people who have a lot of money to invest. Mutual Funds can be invested by anyone and you don’t need to be rich or have a high net worth to invest in them.

# What to Look For in a Child-Saving Plan:

While most parents realize the requirement to save a corpus for the future of their children, they do not fully grasp the nature of what that corpus should account for. Hence, if parents or one parent is earning a sufficient salary at present, enough to support their household and pay for the current educational and other needs of children, the same amount might not suffice in the future.

As inflation may be on a downward trend, the cost of goods and services is still high, and the expenses of the average household in India are only going to grow. For instance, the cost of higher education alone is on the rise, increasing at a rate of 10% to 12% per year. A case in point may be that an average Engineering course costs about Rs. 6 - 7 lakh for four years at present. In a few years, this may increase to Rs. 12 lakh. To take this a step further, if you have plans to send your child abroad for further education, the sky’s the limit at what you may have to spend. Here are some considerations while selecting the best saving plan for a child:

- Consider more than a single plan

- Consider a plan that gives you enough of a corpus for potential educational expenses, health emergencies, and other miscellaneous costs

- Think of the rising rates of inflation and take into account additional expenses for this

- Make a note of your present income and whether you can build some of your future children’s corpus from this

- Consider long-term plans, with assured maturity amounts and as little risk as possible

# Can Minor Invest in Mutual Funds?

Anyone under the age of 18 (minor) can invest in Mutual Funds, with the help of parents/legal guardians until the age of 18. The minor must be the sole account holder represented by the parent/guardian. Joint holding is not allowed in a minor’s Mutual Fund folio. One should have an investment goal for the minor that needs to be achieved by investing in Mutual Funds like say funding higher education.

Once a child attains the age of 18 and becomes a major, the first thing you as a parent/guardian need to do is change the status of the sole account holder from Minor to Major else all transactions would be stopped in the account. The tax implications will now have to be borne by the sole account holder as applicable to any investor above the age of 18 years. Until the child is a minor, all incomes and gains from the child's portfolio is clubbed under the parent's income and the parent pays the applicable taxes. In the year the child turns major, he/she will be treated as a separate entity and will pay taxes for the number of months for which he/she is a major in that year.

# How to plan for your Retirement with Mutual Funds? (Visual Goal Planner Calculator)

Most people don’t think about their retirement until they are close to retirement. The entire working life is spent attending to one requirement after another right from owning a vehicle, a home, raising a family, on kids' education to their weddings. Once these responsibilities have been taken care of, we start looking at how much is left for the retired life that’s around the corner. That’s when people start thinking of investing their life’s savings in something that can give fast returns in a short period before the retirement phase begins. This is the wrong way to plan for that phase of life when you need the most comfort, security, good healthcare, and sustenance over 15-30 years without regular income.

Most people don’t think about their retirement until they are close to retirement. The entire working life is spent attending to one requirement after another right from owning a vehicle, a home, raising a family, on kids' education to their weddings. Once these responsibilities have been taken care of, we start looking at how much is left for the retired life that’s around the corner. That’s when people start thinking of investing their life’s savings in something that can give fast returns in a short period before the retirement phase begins. This is the wrong way to plan for that phase of life when you need the most comfort, security, good healthcare, and sustenance over 15-30 years without regular income.

Planning for this phase must begin as early as possible. Whatever may your earnings and lifestyle be, you can always save the money you have left after paying for all your expenses and fulfilling your financial commitments you surely have some money left at the end of every month after having paid all bills and other liabilities like car EMI, home loan EMI, investment for children, emergency fund, etc. Even if the amount is small, investing this in the right instrument can help you create wealth over the long term. And what better instrument than Mutual Funds? You can invest in mutual funds every month through SIP with as little as Rs. 500 a month and increase the amount as your income/savings grow. You’ll be pleasantly surprised when you see the power of compounding work its magic and who knows you could end up with the proverbial basket of golden eggs!

# How to build a Retirement corpus with Mutual Funds? (SEBI Investor | Retirement Calculator)

Most people don’t realize that their retired lives can be as long as their working life and they’ll need an enormous corpus to last at least 25-30 years. Without proper financial planning, your savings may not be sufficient to cover all expenses and emergency needs. But how do you build a corpus to sustain 25-30 years of retired life? Firstly, figure out what your annual expenses are going to look like after retirement using our Inflation calculator and decide on the total corpus you will need to sustain 25-30 years of your retired life. Once you have the retirement corpus in mind, you can use our Goal SIP Calculator to arrive at the monthly SIP investments you need to start now to be able to build the corpus, you’ve arrived at above, during your working years. The advantage of investing in mutual funds through SIP is that it doesn’t pinch your wallet and can be managed from your monthly income.

Most people don’t realize that their retired lives can be as long as their working life and they’ll need an enormous corpus to last at least 25-30 years. Without proper financial planning, your savings may not be sufficient to cover all expenses and emergency needs. But how do you build a corpus to sustain 25-30 years of retired life? Firstly, figure out what your annual expenses are going to look like after retirement using our Inflation calculator and decide on the total corpus you will need to sustain 25-30 years of your retired life. Once you have the retirement corpus in mind, you can use our Goal SIP Calculator to arrive at the monthly SIP investments you need to start now to be able to build the corpus, you’ve arrived at above, during your working years. The advantage of investing in mutual funds through SIP is that it doesn’t pinch your wallet and can be managed from your monthly income.

Next, choose a few mutual fund schemes for long-term growth depending on your risk appetite. While equity funds are recommended for the long term, you can choose debt or hybrid funds as well. Align your return expectations with the category and type of mutual fund schemes you choose.

Well begun is half done. By bringing in discipline early in the best possible manner, it will take less effort to achieve your financial goal of a happy retired life.

# Why do I need to plan for Retirement if I’ve saved enough? (financial Goal Planner with Variable Asset Allocation)

Whatever may be your current age and financial position, you never know what’s in store for tomorrow. If you aren’t sure about tomorrow, can you be sure that what you’ve saved for retirement will see you through till your last day?

you’ve saved for retirement will see you through till your last day?

Both life expectancy and medical costs are on the rise and you don’t know if your retirement phase is going to last one or three decades. For any financial planning to work effectively, knowing the time horizon is crucial but, in this case, there is no certainty of the time frame. Hence, it’s best to build a surplus into your retirement corpus. But how does one build a surplus when meeting financial goals in the first place is a challenge? You can build a cushion for your retired life by investing your savings in something that has the potential to beat inflation in the long term and create wealth, like Mutual Funds.

A surplus retirement fund saves you from unexpected jerks be it in the form of a medical emergency or any untoward event. Also, you can afford to splurge a bit like gifting your children or grandchildren occasionally to express your love, traveling to meet family and friends more frequently, and pampering yourself with indulgences. It’s never enough to save for retirement if you want to romance with it!

# Is it Wise for Retirees to Invest in Mutual Funds?

Retired people usually have their savings and investments locked up in bank FDs, PPFs, gold, real estate, insurance, pension plans, etc. Most of these options are difficult to convert to cash immediately. This may lead to undue stress in case of medical or other emergencies. Mutual Funds provide much-needed liquidity to retirees as they are easy to withdraw and offer better post-tax returns.

Retired people usually have their savings and investments locked up in bank FDs, PPFs, gold, real estate, insurance, pension plans, etc. Most of these options are difficult to convert to cash immediately. This may lead to undue stress in case of medical or other emergencies. Mutual Funds provide much-needed liquidity to retirees as they are easy to withdraw and offer better post-tax returns.

Most retired people fear the volatility or fluctuation in returns of Mutual Funds and stay away from them. They should put some part of their retirement corpus in Debt Mutual Funds and go for a Systematic Withdraw Plan (SWP). This will help them earn a regular monthly income from such investments. Debt funds are relatively safer than equity funds as they invest in bonds issued by banks, companies, government bodies, and money market instruments (bank CDs, T-bills, Commercial Papers).

SWP in debt funds provides tax-efficient returns as compared to bank FDs. Income from FDs/pension plans is taxed at higher effective rates compared to withdrawals under SWP. You can easily stop a SWP or change the withdrawal amount anytime depending on your need unlike in a pension plan. Thus, retirees should include Mutual Funds in their financial plans.

# Are Debt Funds Suitable for My Financial Goals?

Debt Funds provide lower but relatively stable returns as compared to equity funds. They provide stability to a portfolio as they trade in the fixed-income market which is more stable in comparison to the stock market that impacts equity funds. Everyone needs a financial plan that’s designed to meet various financial goals in the future, like a kid’s college education, medical expenses, house, retirement, etc. We invest our money in different assets like property, gold, stocks, and Mutual Funds to achieve different financial goals that arise at different points in our lives.

education, medical expenses, house, retirement, etc. We invest our money in different assets like property, gold, stocks, and Mutual Funds to achieve different financial goals that arise at different points in our lives.

Debt Funds are most suited for goals that are short-term in nature, as opposed to equity funds that are suitable for long-term goals like retirement planning, given their volatile nature in the short term. Some Debt Funds like Liquid Mutual Funds are suitable for parking your money for a few months if you’ve received a bonus or sold some other investment and are deciding on what next to do with the money. Debt funds are also suitable for goals that you don’t want to take the risk of failing to fulfill it, like the college education money that you want to withdraw in 2 years’ time. You can invest your money in a fixed-income fund for such kinds of goals. Thus, debt funds should be a part of every financial plan.

# Which Mutual Fund should I choose for long-term investments?

Long-term investments aim to finance distant future goals, like college education, home, retirement, etc. Hence, choose a fund suitable for wealth creation. Long-term goals have a horizon beyond 10 years and equity-oriented schemes(>=65% equity allocation) are one of the best long-term investment options. Equities have a higher potential for growth even though more volatile in the short term as compared to hybrid and debt funds. A well-diversified equity fund is more likely to offer stable growth over the long term.

Long-term investments aim to finance distant future goals, like college education, home, retirement, etc. Hence, choose a fund suitable for wealth creation. Long-term goals have a horizon beyond 10 years and equity-oriented schemes(>=65% equity allocation) are one of the best long-term investment options. Equities have a higher potential for growth even though more volatile in the short term as compared to hybrid and debt funds. A well-diversified equity fund is more likely to offer stable growth over the long term.